Admin

We all make monthly budgets. There is an income column; we write all our expected recurring expenses in another column and note down all contingencies that might occur. But how many times did you split your monthly budget into weeks and discover that your weekly budget varies each month? It’s more common than you would like to believe.

Create a Weekly Budget

Here is what I do to save on weekly budgets, factoring in variations.

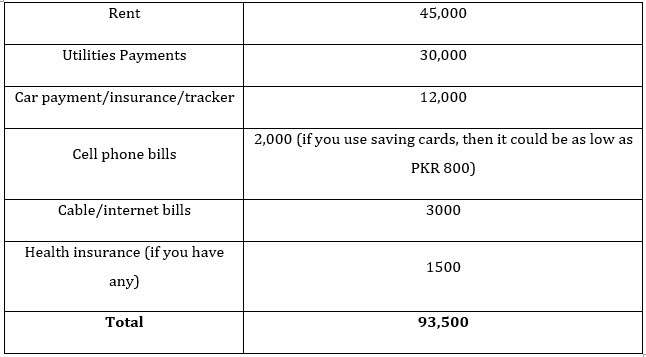

Start with your monthly expenses. Monthly expenses take into account constant/repeat expenses. These are the items you can not afford to miss:

Disclaimer: The calculation above considers the expenses of a person with average earnings. You can replicate the same sheet and use your earnings/spending to project your weekly budget.

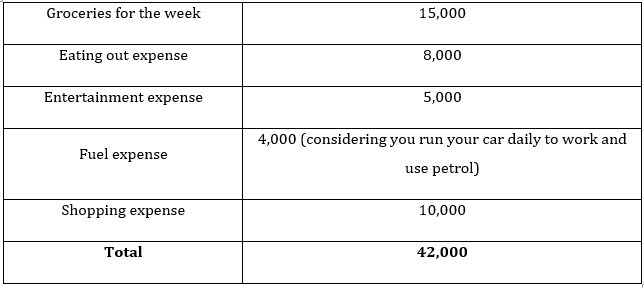

Your weekly budget includes all variable and one-time expenses. For example:

For 4 weeks, the above estimated total expense comes down to Rs. 168k!

To cover both the expenses, that is, the monthly and variable expenses, your income should be more than Rs. 261.5k (168,000 + 93,500). Remember, this is just the expense; there are no savings yet!

So unless you are minting top dollar, you may be unable to spend so much!

How can you make your budget more lifestyle-friendly?

Buy in bulk

The biggest item on most households’ list is food. If you do groceries weekly, buy in bulk so that most of your groceries last a fortnight or even a month. You may not be able to extend the life of perishable items. But dry and processed items can have longer shelf life.

This way you will spend more initially but less or not at all the rest of the month. For fresh items, consider options like freezing and drying.

Get to know food

Another way to cut expenses is to learn and try new recipes at home. Additionally, you can host parties for friends or family to test your new culinary skills.

Consider learning to make coffee and tea in several ways. This will add to your skill set and reduce eating-out expenses.

Shopping

Create a threshold price range for your shopping splurge. If a particular item falls within this range, buy it only then.

Upgrade your closet when you find good discounts. Shopping is hard to resist, but buying at full price will push you out of your budget.

Entertainment

This might contradict all frugal advice for subscriptions, but everyone needs a good entertainment outlet.

Subscribe to Netflix or other similar offers for good in-house video entertainment. For more intellectual options, subscribe to podcasts – they are free!

These options are cheaper. However, if you are the kind who gets hooked, staying away from subscriptions is a good idea. For you, theatres and libraries are a good option.

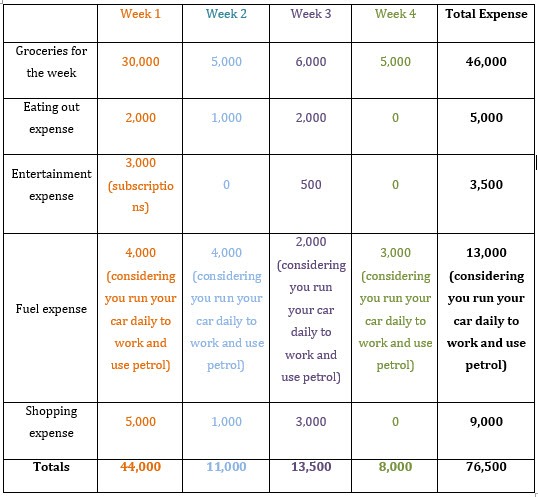

What does the weekly budget look like?

Your variable expense goes down by 54.4%. Add the above total to your recurring monthly total, which comes down to Rs. 167.5k.

Looks way better than the harrowing figure we calculated earlier?

But what if you cannot afford this expense?

Fret not; there is a solution for that, too.

Change is always good

Tone down the constant/repeat expenses. Yes, it will require some effort.

Find a cheaper house to rent. That will bring down the rent and utility payments.

Do away with the car insurance or monthly payments. You may have to give up your car for a while. But this also means no fuel costs and more savings. Also find a cost-effective internet service provider.

However, health insurance is always a good idea. Instead of cutting it out as an unnecessary expense, request your employer do it for you.

Plan for tomorrow

Budgeting works best if you can keep it simple and want to reach your financial goals. But like every budgeting technique, expect weekly budgets to be flawed from the get-go.

You will likely be over budget for the first few weeks, even months. It’s perfectly fine. Let yourself settle in.

The idea is to micromanage each expense bucket, shifting money from unfavorable options to favorable ones. This takes some experimentation and a learning mindset.

So keep at it to make the most of your money!

About the Author

Uroosa Kanwal is a seasoned blogger and writer. She writes on finance and shares tips for women on how to become more financially mindful and aware.